- Home

- Tax Services

For Individuals

For Business

- Family Law

- Real Estate

- Corporate Services

- Business Sales & Acquisition

- Business Incorporations

- Offshore Incorporations

- Contracts and Agreements

- Business Advisory Services

- Reorganizations

- Amalgamations (mergers)

- S.85 Roll-overs

- Butterfly Transactions

- Shareholder Agreements

- Leases

- Succession Planning

- Business Start-up Planning

- Personal Real Estate Corporations (PREC)

- Agreements

- Wills & Estates

- Contact Us

- About Us

Award Winning Tax Lawyers in Toronto – Just 4 Lawyers

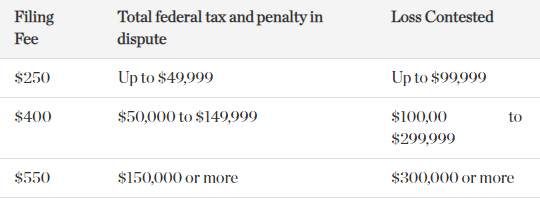

The disputed amount of federal tax and penalties is not more than $25,000 per assessment;

The disputed loss amount is not more than $50,000 per determination or

Interest on federal taxes Audit and on penalties is the only matter in dispute